In 2026, the landscape of payment methods for Australian businesses has moved far beyond simple card transactions. For small business owners and operations leads, staying competitive now means navigating a digital-first environment shaped by evolving RBA surcharging rules and rising consumer expectations.

While many still rely on legacy bank transfers, payment providers are shifting toward faster, more integrated options like PayTo, PayID, and secure payment links.

ZenPay simplifies the landscape by offering a versatile range of payment options for Australian businesses, allowing you to collect revenue faster through a single, integrated platform:

· Card & Digital Wallets: Visa, Mastercard, Apple Pay, and Google Pay.

· Modern Instant Payments: PayTo and PayID.

· Strategic Links: Secure, one-click payment links for remote billing.

· Traditional Methods: Automated Direct Debit and Bank Transfers (EFT).

· Global Reach: Alipay+ and UnionPay

By combining these options, ZenPay removes payment friction and ensures your business is ready for the digital-first economy of 2026.

Card Payments: Visa, Mastercard, AMEX, the baseline and what to consider

Despite shifting trends, card payments remain the baseline for payment methods for Australian businesses, accounting for roughly 75% of all transactions.

Accepting Visa, Mastercard, and Amex streamlines your operations by providing a secure digital record to protect against disputes while ensuring predictable cash flow through rapid deposits. By offering customers the flexibility to pay how they prefer on a single platform, you facilitate faster payments and a more seamless checkout experience.

However, the landscape is changing as new 2026 surcharging regulations have restricted merchants’ ability to pass on

costs, potentially making cards a less attractive option compared to newer alternatives. To maintain margins under these rules, forward-thinking businesses are now looking toward integrated solutions that balance card convenience with lower-cost digital methods such as PayID or PayTo.

Apple Pay and Google Pay: Why customers increasingly prefer them

Digital wallets like Apple Pay and Google Pay have become the default choice for many Australians. In a single month in 2024 alone, Australians made over 500 million digital wallet transactions, moving more than AUD $20 billion. For practice managers and operations leaders, this shift is driven by the speed and biometric security these methods offer, providing customers with a seamless one-tap experience that reduces checkout friction.

Beyond customer preference, adopting these digital payment solutions allows your business to move toward faster, more secure financial operations. These platforms offer high-level features like real-time payment tracking and cost-saving multi-currency capabilities, which are essential for small businesses. Because these wallets integrate easily with your existing accounting software, they simplify the entire reconciliation process and financial analysis, ensuring your backend is just as efficient as your front-end payment experience.

PayTo

What is PayTo?

PayTo is a secure, real-time payment method built on the New Payments Platform (NPP) that modernises traditional direct debit. Instead of manual forms, your business sends a digital payment agreement directly to the customer’s banking app for instant approval.

This digital-first approach gives customers total control to view or pause agreements within their own bank’s secure platform, while providing your business with immediate fund clearance. Whether for one-off transactions or recurring subscriptions, PayTo offers a fast, transparent, and reliable alternative to both credit cards and legacy banking.

How PayTo works

PayTo streamlines the payment process into a three-step digital workflow that offers significantly more control than traditional direct debit. To get started, your business must be sponsored as a PayTo User through a payment service provider. Once enabled, you can initiate a sale by creating a PayTo agreement, a digital record detailing the amount, frequency, and duration of the payments, whether they are one-off, ad-hoc, or recurring.

The process follows a transparent path for the customer:

1. Selection: The customer selects PayTo as their payment option.

2. Authorisation: The agreement is sent directly to the customer’s mobile or internet banking app, where they review and approve the

terms instantly.

3. Initiation: Once authorised, the payment is processed via the NPP, which performs real-time validation and

funds-availability checks.

Because all records are stored in a centralised NPP database, both you and your customer receive instant notifications if an agreement is paused, amended, or cancelled. This real-time visibility eliminates the guesswork of legacy banking, providing immediate confirmation of transaction success and ensuring your records are always accurate.

Why it matters for your business

As the 2026 RBA surcharging changes make it harder to pass on high card fees to your customers, PayTo emerges as the most strategic alternative for protecting your margins. It shifts your business from a high-fee “card-first” model to a high-margin “account-first” model.

- Protect Your Margins: With the ability to surcharge cards being restricted, PayTo’s low, flat-fee structure ensures you keep more of every dollar without needing to add extra costs at checkout.

- Instant Certainty: Receive real-time confirmation of payment success, eliminating the days of uncertainty and dishonour fees associated with legacy systems.

- Reduced Admin: Real-time notifications and rich data capabilities automate reconciliation. You are alerted instantly if a customer pauses or changes an agreement, so your books stay accurate without manual effort.

- Enhanced Security: Authorisation happens directly within the customer’s secure banking app. This drastically reduces fraud risk and unauthorised debits compared to traditional methods.

- 24/7 Processing: Unlike traditional banks or legacy BECS, PayTo operates continuously, including weekends and public holidays, ensuring your cash flow never pauses

PayID

PayID, a powered NPP, has transformed real-time bank transfers by replacing BSB and account numbers with simple identifiers like a phone number, email, or ABN. With over 27 million PayIDs created in Australia and nearly AU$2 trillion moved annually in real-time transfers, this method has quickly become a standard for secure, instant payments. When a customer enters your PayID into their banking app, they receive immediate confirmation of your business name, providing the peace of mind that funds are going to the right place.

· Zero Surcharge Stress: Because PayID doesn’t rely on the card schemes targeted by the RBA ban, you avoid the dilemma of absorbing card fees or raising your sticker prices. You keep 100% of the sale.

· Near-Instant Liquidity: PayID transfers typically arrive in under a minute via Osko, ensuring your cash flow remains fluid 24/7.

· Built-in Security & Trust: PayID eliminates the need to share sensitive bank details. Customers see your business name before they pay, which reduces both fraud risk and checkout hesitation.

· Automated Admin: Digital-first identifiers allow for faster, more accurate reconciliation, saving your operations team hours of manual data matching.

By adopting PayID now, you are progressing your business with a payment method that is as profitable for you as it is easy for your customers.

Direct Debit: best for recurring payments, memberships and instalments

Direct Debit remains a cornerstone payment method for Australian businesses managing memberships, instalments, and long-term payment schedules. By allowing you to collect funds automatically on set dates, it provides a dependable way to predict cash flow and ensures you never have to worry about chasing overdue invoices again. This “set and forget” approach is ideal for fixed recurring payments, offering a proven method to maintain consistent revenue without the administrative burden of manual follow-ups.

The primary advantage of direct debit is a simplified back-end, where it reduces paperwork and offers flexible scheduling, allowing you to align billing with your specific service cycles. By automating the collection process, you significantly simplify reconciliation and remove the friction of traditional billing, ensuring your business keeps moving while your clients enjoy a seamless, uninterrupted service experience

Payment Links: collecting payment via email or SMS without a terminal

ZenPay’s Payment Link provides a simple way to collect revenue without the need for a physical terminal or a face-to-face interaction. By sending a secure payment request via email or SMS, you provide customers with a personalised payment page where their name, contact details, and the billing amount are already prepopulated. This pre-filled approach removes manual entry errors and significantly reduces payment friction, making it far more likely that your invoices are settled on time.

For your operations team, this method simplifies the entire collection cycle from end-to-end. Once the customer pays, you receive an instant notification, and the transaction is immediately visible in your merchant portal. It is the ideal solution for service businesses looking to offer professional, remote billing that is as fast for the business as it is easy for the client.

Bank transfer/EFT: still common, but slow, and what replaces it

While traditional EFT is a common fixture, it is increasingly a bottleneck for modern operations. Relying on BSB and account numbers often leads to manual entry errors and multi-day settlement delays. For operations leads, the biggest hurdle is manual reconciliation as this process drains administrative time and leaves cash flow in limbo.

Modern alternatives like PayID and PayTo are now replacing legacy EFT. These methods offer the same account-to-account security but with instant settlement and automated reconciliation. By switching to these NPP-powered solutions, you gain real-time confirmation and rich data, moving your business toward a faster, more automated financial workflow

Asian payment wallets: Alipay, Union Pay, relevant for businesses serving international clients

What is Alipay+?

Alipay+ is a global network that connects local merchants to millions of international consumers. It allows customers to pay via their preferred home wallet using familiar QR codes, while you receive settlement locally through ZenPay without needing separate foreign currency accounts.

What is UnionPay?

As one of the world’s largest card networks, UnionPay is the primary payment method for Chinese consumers globally. Accepting UnionPay through ZenPay allows you to tap into a massive cardholder base, catering to international students, tourists, and residents who specifically seek out UnionPay-friendly merchants.

How this can help businesses with international clients

Australia’s strong economic, education, and tourism links to Asia make localised payment methods for Australian businesses a strategic necessity for growth. Consumers are far more likely to complete a purchase and make faster decisions when they see trusted, familiar options at checkout, significantly reducing cart abandonment and hesitation.

By integrating these wallets through ZenPay, you can serve a broader cross-border customer base with unparalleled scale. We help you boost conversion rates by removing friction and offering cost-effective, easy-to-integrate capabilities that span borders and devices. Offering these preferred methods makes it easier for your international clients to pay, ensuring it is even easier for you to get paid.

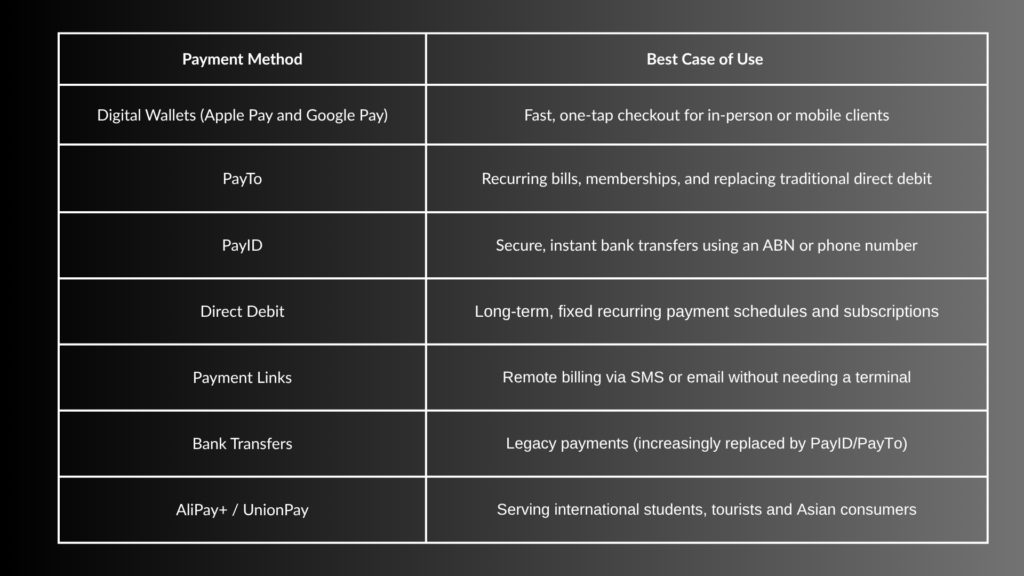

Comparison Table: Best use case per method

ZenPay supports all these payment methods in one platform. Talk to our team today about the right setup for your business.